Your Banking Identity Exists. The Systems Disagree.

EXPAT BANKING

Blog > Expat Banking > Your Banking Identity Exists. The Systems Disagree.

Your Banking Identity Exists. The Systems Disagree.

EXPAT BANKING

BANKEAZ | Expats Team

7/06/2026 - 4 min read

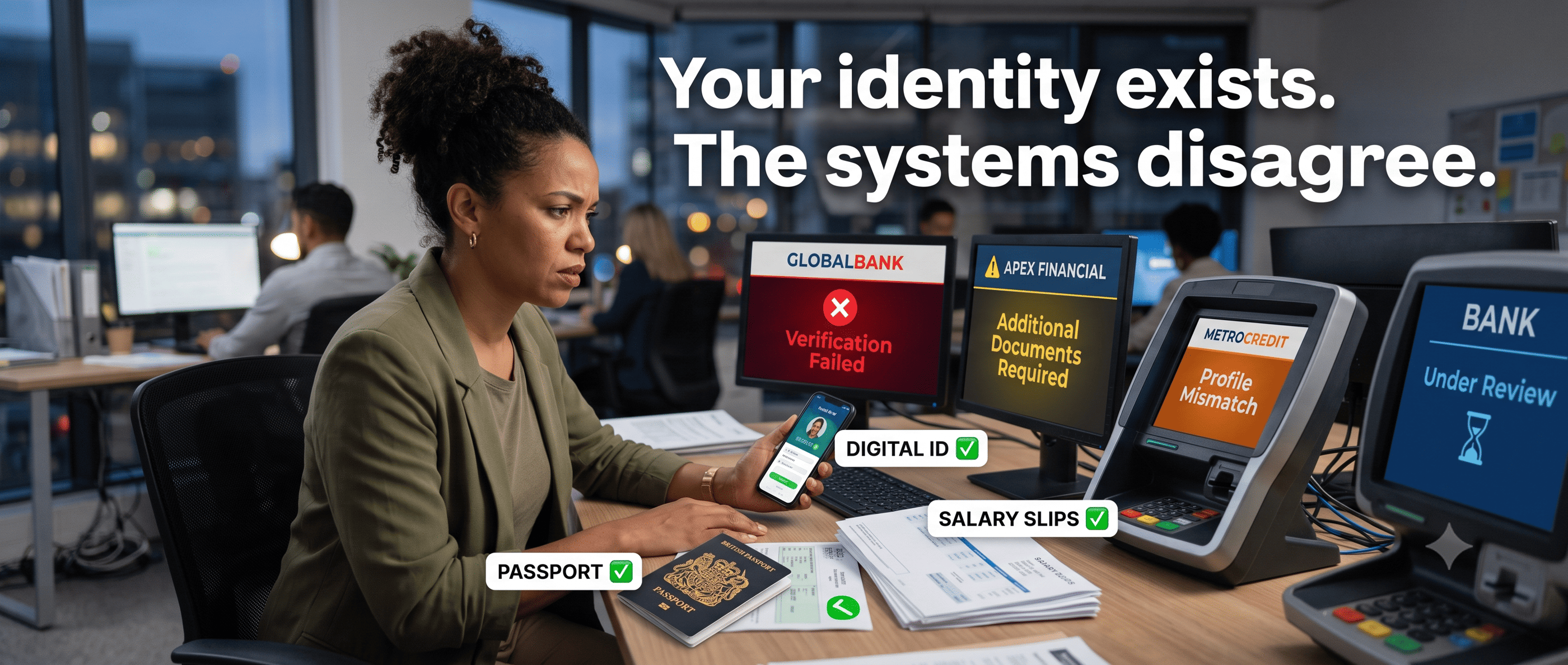

Your identity exists, but your bank may still treat it like a question.

That is one of the most frustrating expat banking problems today. People move, work, study, invest, and support families across borders. Yet many banking systems still depend on local proof, local addresses, and local risk models.

The main issue is simple: international banking has not fully adapted to mobile lives. Your passport, income, and financial history may be valid, but different systems often fail to recognize them together.

That is why cross-border banking can feel broken. The person is real. The money is real. The systems do not agree.

You live internationally. Your bank should too.

Manage your money across countries without hidden fees, delays, or complexity.

Simplify your financial life abroad with Bankeaz.

Banking built for life between countries

Free early access

> Why does your banking identity break across borders?

Banking identity is still built around local assumptions.

A bank often wants a domestic address, local tax details, local credit history, and documents issued in the same country. When you relocate, those signals change.

You may still be the same person. But to the bank, your profile can suddenly look incomplete.

This is why many mobile customers struggle with international banking. The problem is not identity itself. The problem is recognition.

People have become global. Banking has not.

> What Happens Behind the Transfer?

The impact is practical and immediate.

You may face repeated KYC checks. Your transfer may be blocked. Your card may stop working. Your account may even be reviewed or closed after relocation.

These are not small inconveniences.

They affect rent, salaries, tuition, savings, insurance, and family support. A delayed payment can become a missed deadline. A blocked transfer can become a financial emergency.

For many people searching for banking for expats, the real need is continuity. They want access to money without restarting their financial life every time they move.

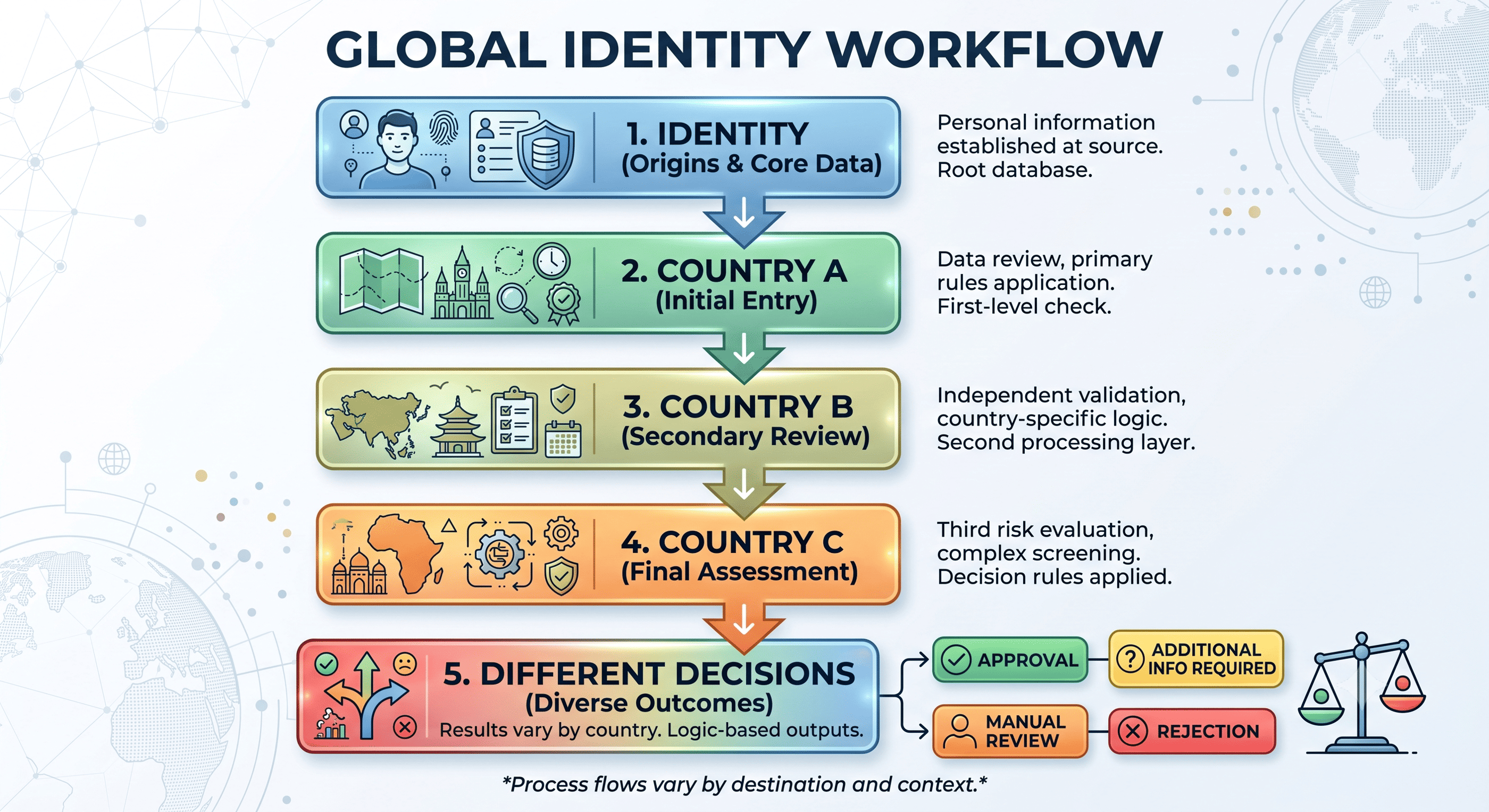

> Why are cross-border checks so repetitive?

Banks operate under strict rules.

They must know who their customers are, where funds come from, and whether activity creates risk. That is necessary for financial security.

But the process is often fragmented.

One bank may accept a document. Another may reject it. One country may recognize a digital proof. Another may still require a local utility bill.

According to the FATF ↗, financial institutions should apply a risk-based approach to customer due diligence, meaning controls should match the level of risk rather than treat every case the same.

In practice, mobile customers are still often treated as exceptions.

Banking still treats mobility as an exception.

> How do proof of address rules create exclusion?

Proof of address is one of the biggest barriers in cross-border banking.

Many expats do not have a utility bill when they first arrive. Some live in temporary housing. Others use employer accommodation or shared rentals.

Yet banks often ask for exactly the documents newcomers do not yet have.

This creates a loop.

You need a bank account to settle. But you need local proof to open or keep the bank account. The system asks for stability before it gives you access to financial stability.

The result is lost time, limited access, and reduced mobility.

> Why does this matter for diaspora communities?

Diaspora communities often live financially across more than one country.

They may earn in one currency, save in another, and support family elsewhere. They may need to send money regularly, manage obligations back home, or keep financial ties across borders.

That creates a different banking reality.

For users of diaspora banking, identity is not only about where they live today. It is also about where their money, family, and responsibilities are connected.

When systems disagree, diaspora users pay the price through delays, fees, uncertainty, and limited financial control.

______________________________________________________________________________________________________________________________________________________

> What will make banking identity portable?

The future of banking will depend on financial portability.

Digital identity can help customers prove who they are across borders. Interoperable systems can reduce repeated checks. Global payments can make money movement faster and more predictable.

But innovation must connect identity, compliance, and access.

A portable financial identity would not remove regulation. It would make regulated access easier for people who move.

The goal is simple: your banking profile should travel with you as reliably as your passport.

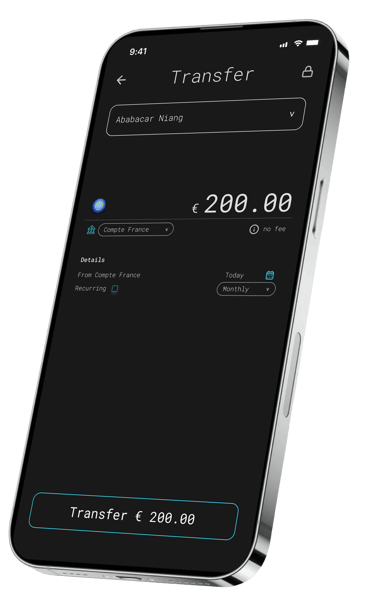

You send money.

You lose part of it.

But you never see exactly where.

International Transfers

> Conclusion

The problem is not that people lack identity. The problem is that banking systems often fail to recognize identity across borders.

That creates blocked transfers, repeated checks, proof of address barriers, and account disruption. It costs people money, time, access, mobility, and financial security.

The future will move toward digital identity, interoperable systems, global payments, and financial portability.

Memorable takeaway: your life may be international, but your bank still thinks locally.

Your identity already travels with you.

Your banking should too.

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

Country

____________________

Europe ↗

Italy ↗

Germany ↗

France ↗

__________________________________________________________________________________________________________________________________________________

Africa ↗

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________