Why Your Transfer Stays “Pending” for Days

EXPAT BANKING

Blog > Expat Banking > Why Your Transfer Stays “Pending” for Days

Why Your Transfer Stays “Pending” for Days

EXPAT BANKING

BANKEAZ | Expats Team

5/11/2026 - 4 min read

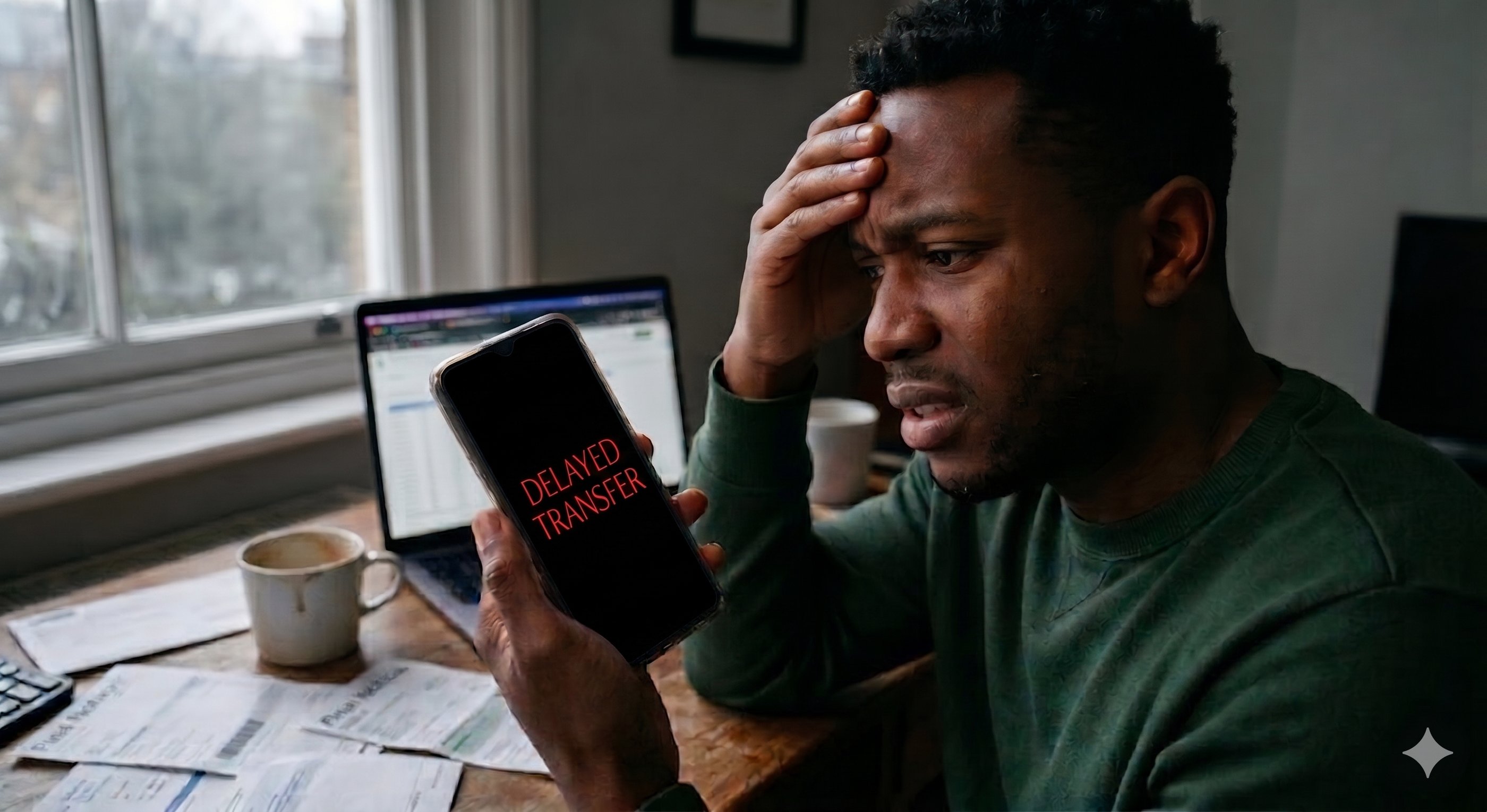

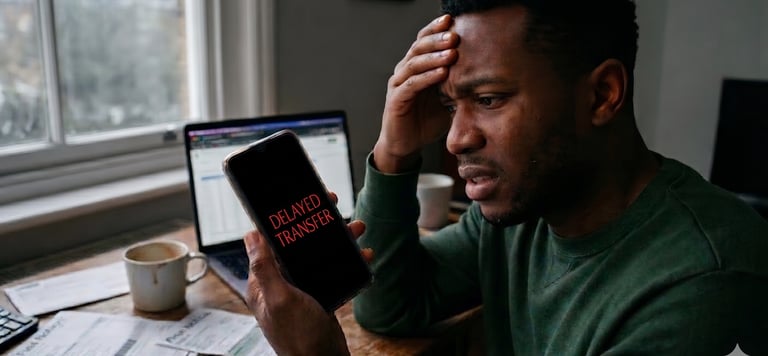

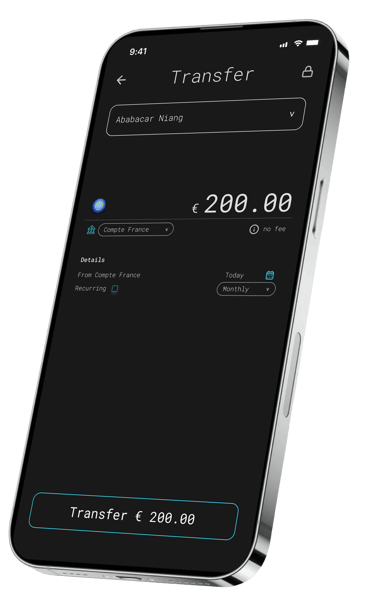

International transfers often look simple.

You send money and expect it to arrive quickly.

Instead, the payment stays “pending” for days.

This is one of the most common expat banking problems in modern international banking.

Behind the delay, multiple banking systems, compliance checks, and cross-border intermediaries interact at the same time.

You live internationally. Your bank should too.

Manage your money across countries without hidden fees, delays, or complexity.

Simplify your financial life abroad with Bankeaz.

Banking built for life between countries

Free early access

> Multiple Banks Process One Transfer

A cross-border transfer rarely moves directly from one bank to another.

Most payments pass through intermediary banks before reaching the final account.

Each institution performs its own checks and processing cycle.

This creates delays in cross-border banking, especially when banks operate in different time zones.

Learn more about international banking.

> Compliance Checks Slow Payments

Banks must verify transactions for anti-money laundering rules and fraud prevention.

A transfer can be paused automatically if information appears incomplete or unusual.

Large international payments often trigger additional reviews.

This is a major source of expat banking problems, especially for migrants and remote workers moving money frequently.

> Currency Conversion Adds Delays

Transfers involving currency exchange require extra settlement steps.

Some banks convert currencies instantly.

Others wait for internal processing windows before completing the exchange.

This increases waiting times in international banking, particularly during weekends and holidays.

Discover more about banking for expats.

> Different Banking Networks Operate Separately

Not all countries use the same banking infrastructure.

Some payments travel through SWIFT networks.

Others depend on domestic clearing systems with limited operating hours.

This fragmentation creates friction in cross-border banking and slows global transfers.

> Missing Information Can Freeze a Transfer

Incorrect beneficiary names, incomplete IBAN numbers, or missing addresses can stop a payment automatically.

Banks may hold the transfer until the sender provides new information.

For globally mobile users, this becomes a recurring operational issue in international banking.

Explore modern diaspora banking.

______________________________________________________________________________________________________________________________________________________

> Legacy Banking Systems Still Dominate

Many international banks still rely on outdated infrastructure.

Manual verification processes remain common.

Real-time processing is not available everywhere.

As global mobility increases, these limitations continue to create major expat banking problems for users managing money across borders.

According to the Bank for International Settlements ↗, cross-border payment systems remain fragmented and costly in many regions.

> Conclusion

Global banking is evolving slowly while international mobility grows rapidly.

Users now expect faster and more transparent financial systems.

Yet many traditional institutions still depend on fragmented infrastructures designed decades ago.

Modern cross-border banking must reduce delays, simplify compliance, and improve transparency for globally mobile users.

You send money.

You lose part of it.

But you never see exactly where.

International Transfers

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

Country

____________________

Europe ↗

Italy ↗

Germany ↗

France ↗

__________________________________________________________________________________________________________________________________________________

Africa ↗

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________