Why International Payments Pass Through So Many Banks

EXPAT BANKING

Blog > Expat Banking > Why International Payments Pass Through So Many Banks

Why International Payments Pass Through So Many Banks

EXPAT BANKING

BANKEAZ | Expats Team

6/29/2026 - 4 min read

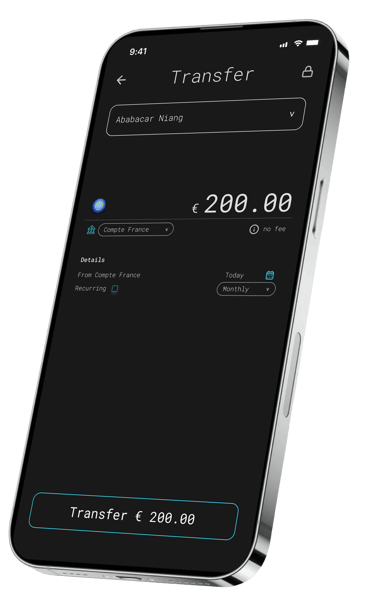

Your money can cross a border in seconds, but the banking system behind it often moves through a maze.

This is why international payments may pass through several banks before reaching the final account. The sender’s bank and the receiver’s bank often do not have a direct relationship, so intermediary banks help route, verify, convert, and settle the payment.

For people living abroad, this creates real expat banking problems.

A transfer that looks simple on an app can become complex inside the global financial system. International banking still depends on networks, regulations, currencies, and compliance checks built around national banking systems.

That is why cross-border banking often feels slower, more expensive, and less predictable than domestic banking.

You live internationally. Your bank should too.

Manage your money across countries without hidden fees, delays, or complexity.

Simplify your financial life abroad with Bankeaz.

Banking built for life between countries

Free early access

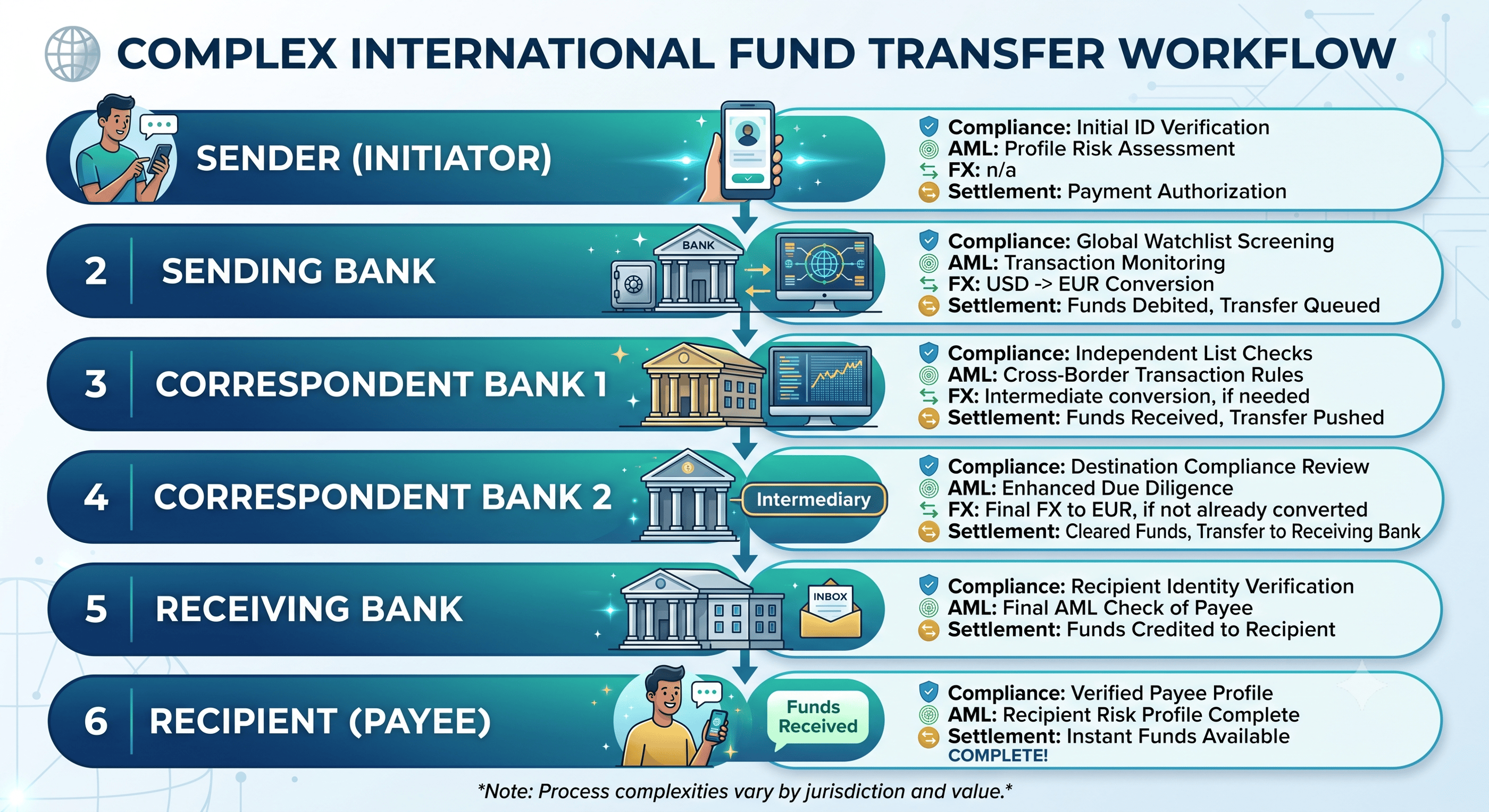

> Why Do International Payments Need Intermediary Banks?

International payments usually need intermediary banks because not every bank is directly connected to every other bank.

A local bank in France may not have a direct account relationship with a bank in Kenya, Canada, India, or Brazil. So the payment moves through correspondent banks that can connect both sides.

These banks help move funds across jurisdictions, currencies, and settlement systems.

In simple terms, they act like bridges.

This is a core reason why international banking can feel invisible until something goes wrong.

> What Happens Behind the Transfer?

When you send money abroad, several things happen behind the screen.

The bank checks the sender.

It checks the recipient.

It checks the destination country.

It checks sanctions, fraud risk, currency details, and payment instructions.

Then the payment may move through one or more correspondent banks before arriving at the recipient’s bank.

Each bank may review the transaction.

Each bank may charge a fee.

Each bank may create delay.

According to the BIS CPMI ↗, cross-border payments often face frictions linked to fragmented data standards, different operating hours, compliance checks, and long transaction chains, which can increase cost and delay.

> Why Can Payments Get Delayed or Blocked?

Payments can get delayed when the information is incomplete, inconsistent, or flagged for review.

A missing middle name, old address, unclear purpose of payment, or mismatch between bank records can trigger checks.

For expats, this is common.

You may open an account abroad, change your phone number, use a foreign address, or receive income from another country. Then your bank asks for proof of address again.

Sometimes the transfer is paused.

Sometimes the account is restricted.

Sometimes the money returns after days, minus fees.

These are everyday expat banking problems, not rare exceptions.

> Why Do Fees Appear Along the Way?

nternational payment fees often appear because multiple banks may touch the transaction.

Your bank may charge a sending fee.

An intermediary bank may deduct a handling fee.

The receiving bank may charge an incoming fee.

Currency conversion can add another cost.

The problem is that customers often do not see the full route before sending money. They only discover the final amount when it arrives.

For anyone using banking for expats, this creates uncertainty.

Money leaves one account, passes through several systems, and arrives smaller than expected.

> Why Is This Harder for Mobile People?

Banking still treats mobility as an exception.

That is the core problem.

People move for work, study, family, safety, business, and opportunity. But bank accounts, credit histories, identity checks, and payment systems are still mostly national.

An expat may have income in one country, rent in another, savings in a third, and family support obligations somewhere else.

This creates pressure on time, money, access, and financial security.

A delayed rent payment can damage trust.

A blocked transfer can leave a family waiting.

An account closure after relocation can cut someone off from their own money.

______________________________________________________________________________________________________________________________________________________

> How Is Cross-Border Banking Changing?

The future of cross-border banking is moving toward faster payments, better digital identity, and more interoperable systems.

Banks, fintech companies, and payment networks are working on ways to reduce friction between countries.

Digital identity could make repeated KYC checks easier.

Global payment systems could reduce the number of intermediaries.

Financial portability could let people keep access to banking services as they move.

The goal is simple: banking should move with people, not trap them inside borders.

This is especially important for diaspora banking, where people often need to support families, businesses, and communities across countries.

You send money.

You lose part of it.

But you never see exactly where.

International Transfers

> Conclusion

International payments pass through many banks because the global banking system is still fragmented.

Banks need intermediaries to connect accounts, currencies, regulations, and settlement systems. But this creates delays, fees, blocked transfers, and uncertainty for people who live globally.

The future belongs to banking systems that move as easily as people do.

Your money crosses borders.

Your banking should do it just as smoothly.

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

Country

____________________

Europe ↗

Italy ↗

Germany ↗

France ↗

__________________________________________________________________________________________________________________________________________________

Africa ↗

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________