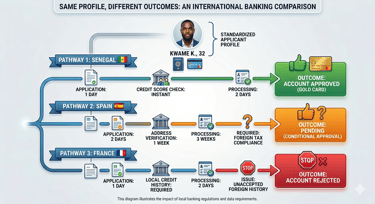

Why Banks Treat the Same Profile Differently

EXPAT BANKING

Blog > Expat Banking > Why Banks Treat the Same Profile Differently

Why Banks Treat the Same Profile Differently

EXPAT BANKING

BANKEAZ | Expats Team

5/14/2026 - 4 min read

A customer can appear reliable in one country and risky in another.

The same income, identity, and financial history may receive completely different treatment across banks.

This is one of the most frustrating expat banking problems in modern international banking.

Different regulations, risk models, and banking systems create inconsistent decisions in cross-border banking.

You live internationally. Your bank should too.

Manage your money across countries without hidden fees, delays, or complexity.

Simplify your financial life abroad with Bankeaz.

Banking built for life between countries

Free early access

> Risk Policies Differ Between Banks

Each bank builds its own internal risk framework.

Some institutions prioritize local financial history.

Others focus on income origin, residency status, or transaction behavior.

This creates inconsistent experiences in international banking, especially for globally mobile users.

Learn more about international banking.

> Residency Status Changes Risk Evaluation

Temporary visas, foreign addresses, or multi-country activity can increase compliance reviews.

Even financially stable customers may face account restrictions or additional verification requests.

For migrants and expats, residency status remains a major source of expat banking problems.

> Credit History Does Not Transfer Internationally

Most countries operate separate credit systems.

A strong financial profile in one region may not exist in another banking database.

This fragmentation affects approvals, lending access, and onboarding in cross-border banking.

Discover more about banking for expats.

> Compliance Rules Vary Across Jurisdictions

Banks must follow national anti-money laundering and financial reporting laws.

Requirements differ from one country to another.

Some institutions apply stricter controls for international customers.

This creates operational friction in international banking for users managing finances across borders.

> Income Sources Are Interpreted Differently

Remote work, freelance income, and international payments are not evaluated equally everywhere.

Some banks classify these profiles as unstable, even when income is regular.

Globally mobile workers often face recurring expat banking problems because traditional systems were built around domestic employment models.

Explore modern diaspora banking.

______________________________________________________________________________________________________________________________________________________

> Legacy Systems Limit Customer Portability

Most banks still operate on national infrastructures designed for local customers.

Cross-border financial identity remains fragmented.

As a result, users must repeatedly prove their legitimacy in different countries.

According to the World Bank ↗, financial inclusion challenges remain significant for internationally mobile populations.

> Conclusion

Global mobility is increasing faster than banking modernization.

Users now live, work, and earn income across multiple countries.

Yet many financial institutions still assess customers through isolated national systems.

Modern cross-border banking must create portable financial identities that reduce friction for globally mobile users.

You send money.

You lose part of it.

But you never see exactly where.

International Transfers

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

Country

____________________

Europe ↗

Italy ↗

Germany ↗

France ↗

__________________________________________________________________________________________________________________________________________________

Africa ↗

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________