Why Banking Decisions Change Abroad

EXPAT BANKING

Blog > Expat Banking > Why Banking Decisions Change Abroad

Why Banking Decisions Change Abroad

EXPAT BANKING

BANKEAZ | Expats Team

6/25/2026 - 4 min read

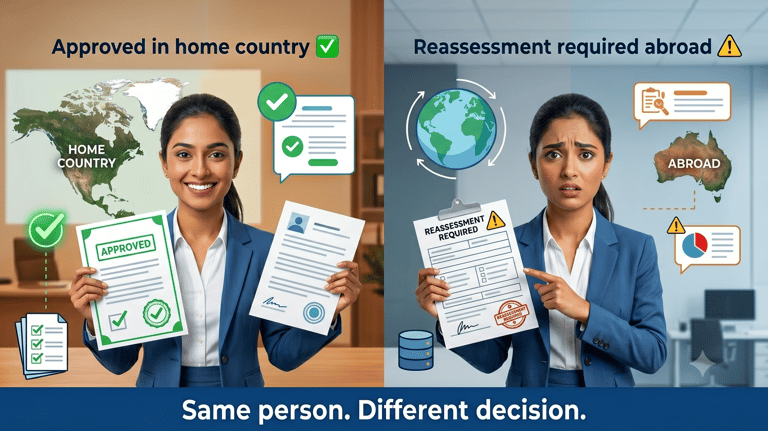

Your bank may trust you at home and question you abroad.

That is one of the most frustrating expat banking problems. You do not become a different person when you move. But your banking profile often changes overnight.

A new country can change how banks assess your address, income, tax status, documents, transaction patterns, and risk level.

This is why international banking often feels inconsistent. The same customer can look low-risk in one country and difficult to verify in another.

The answer is simple: banking decisions change when you move abroad because most banks are built around local rules, local identity systems, and national risk models. That makes cross-border banking harder for people whose lives no longer fit inside one country.

You live internationally. Your bank should too.

Manage your money across countries without hidden fees, delays, or complexity.

Simplify your financial life abroad with Bankeaz.

Banking built for life between countries

Free early access

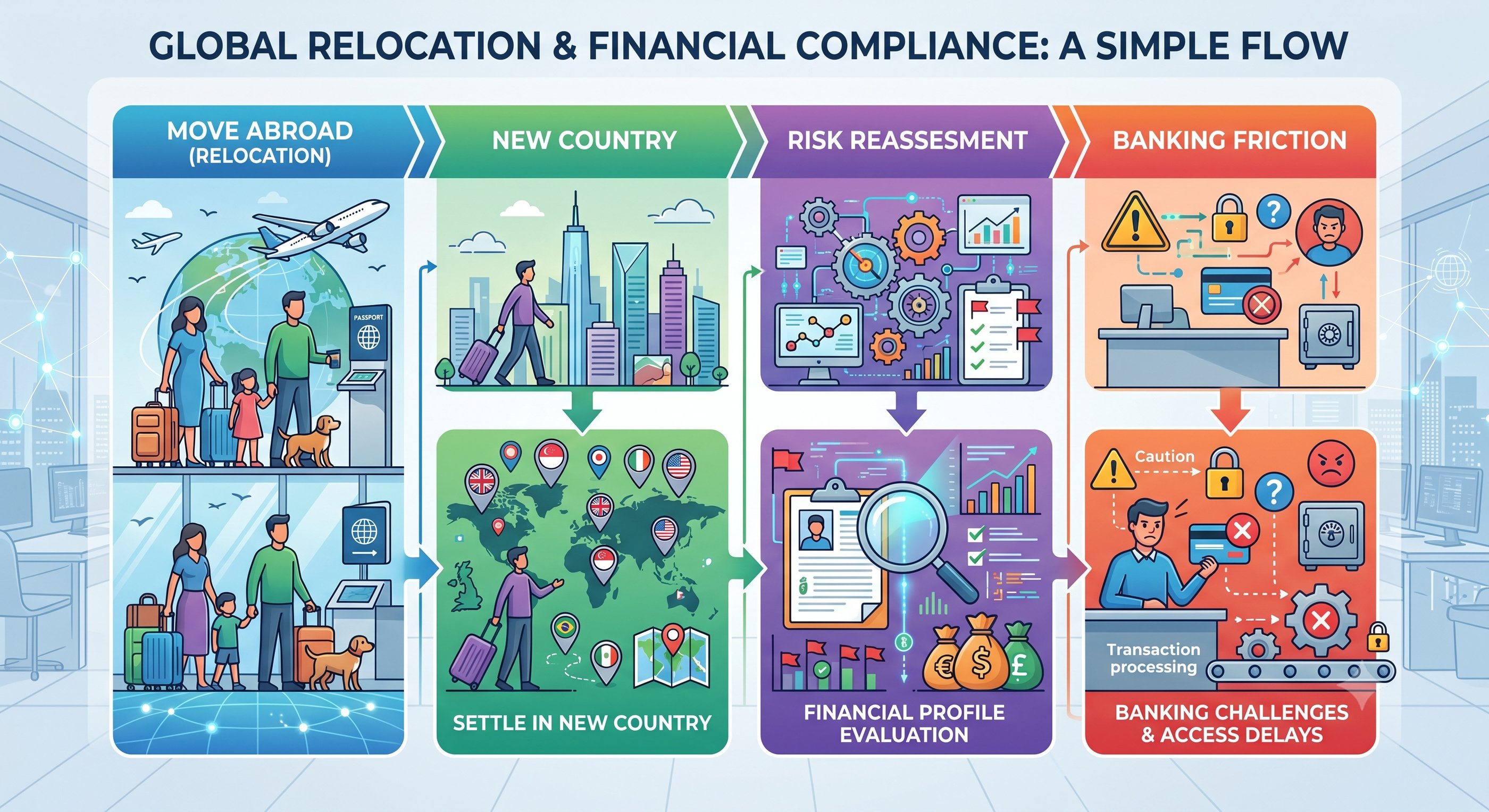

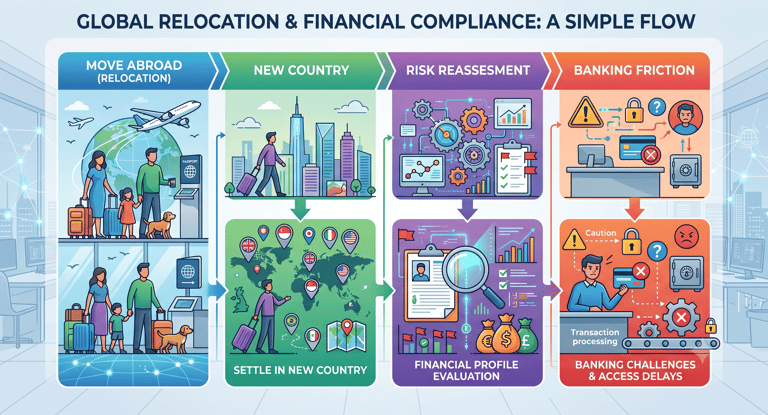

> Why Does Your Bank Reassess You After Relocation?

Banks make decisions based on location.

Your country of residence affects compliance rules, tax reporting, identity checks, and account eligibility. When you move abroad, your bank may need to reassess whether it can still serve you.

That reassessment can feel personal. Usually, it is structural.

A bank may ask for updated documents, new proof of address, or information about foreign income. In some cases, it may restrict features or close the account.

This is why banking for expats needs to be designed around movement, not only residence.

> Why Does Proof of Address Become a Barrier?

Proof of address is one of the most common obstacles abroad.

Many banks ask for a utility bill, rental contract, or official local document before opening an account. But newcomers may not have those documents yet.

This creates a loop.

You may need a bank account to rent an apartment. But you may need an apartment to open a bank account.

That single requirement can delay salary payments, rent deposits, tuition payments, and access to basic services.

For many people, expat banking problems begin with one missing document.

> Why Do Transfers Get Blocked or Delayed?

Moving abroad changes your transaction pattern.

A transfer from a new country, a payment in a new currency, or money sent to family overseas may trigger extra checks. Banks are required to monitor unusual activity, even when the activity is legitimate.

The problem is that global lives often look unusual to national banking systems.

According to the FATF ↗, financial institutions must apply customer due diligence measures to identify and verify customers and understand the purpose of business relationships.

That helps fight financial crime. But for mobile customers, it can also mean repeated KYC checks, delayed payments, or blocked transfers.

> Why Does Credit History Not Travel Easily?

Credit history is usually local.

You may have years of responsible banking in one country. But when you move, another bank may not see that history. It may treat you as financially new.

This affects access.

You may struggle to get a credit card, overdraft, mortgage, loan, or even a standard account package. Your past financial behavior may be real, but not portable.

That is a major weakness in cross-border banking.

People can move countries faster than their financial reputation can follow.

> What Is the Real Impact on Expats?

The impact is practical.

Money can get stuck. Payments can arrive late. Accounts can be limited. Salary access can be delayed. Savings may sit in the wrong currency.

There is also stress.

When banking access becomes uncertain, people lose time and control. They spend hours explaining their situation to support teams, uploading the same documents, and waiting for manual reviews.

This affects mobility, financial security, and confidence.

For globally mobile people, banking friction is not an inconvenience. It is a barrier to living normally.

______________________________________________________________________________________________________________________________________________________

> How Will Banking Decisions Become More Portable?

Banking is slowly moving toward portability.

Digital identity, interoperable payment systems, stronger global compliance tools, and faster payment networks are changing expectations. The future of international banking is not just online access. It is financial continuity across countries.

Better systems could allow people to carry verified financial identity, account access, and payment capability across borders more easily.

This matters for expats, migrants, remote workers, international families, and diaspora banking users.

The future belongs to banking systems that move as easily as people do.

You send money.

You lose part of it.

But you never see exactly where.

International Transfers

> Conclusion

Traditional banking still stops at borders because it was designed for national lives.

But people no longer live, work, study, earn, or support family in only one country. Banking needs to evolve toward digital identity, interoperable systems, global payments, and financial portability.

The memorable takeaway is simple:

People no longer live within one country. Banking should not either.

Your life crosses borders.

Your banking should too.

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

Country

____________________

Europe ↗

Italy ↗

Germany ↗

France ↗

__________________________________________________________________________________________________________________________________________________

Africa ↗

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________