Why living between two countries confuses traditional banks

EXPAT BANKING

Blog > Expat Banking > Why living between two countries confuses traditional banks

Why living between two countries confuses traditional banks

EXPAT BANKING

BANKEAZ | Expats Team

3/16/2026 - 3 min read

Millions of people now live, work, and manage money across borders.

Yet many still experience expat banking problems because traditional banking systems were built for local lives rather than global mobility.

As international careers, remote work, and global families become more common, financial lives increasingly span multiple countries.

However, most traditional banking systems still assume customers live and operate financially in only one place.

#ExpatBanking #CrossBorderBanking

> The reality of global lives

International mobility is increasing rapidly. Professionals relocate for work, students study abroad, and diaspora communities support relatives in other countries. According to the United Nations ↗, more than 304 million people live outside their country of birth.

For these globally mobile individuals, finances often span multiple financial systems. Income may come from one country, while expenses occur in another. International transfers, currency conversions, and foreign payments become routine.

However, traditional banking infrastructure was never designed for this type of cross-border banking activity.

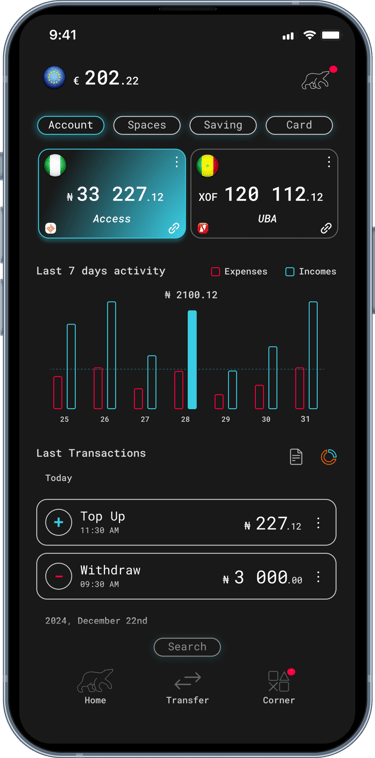

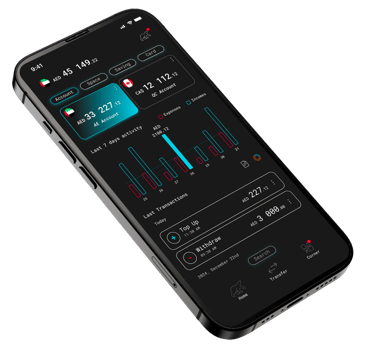

All your accounts. One place.

Connect your external bank accounts to Bankeaz and manage all your money in one place.

U N I O N

> Why traditional banks expect stability

Most banking systems were designed around a simple assumption: customers live and operate financially in one country. Banks typically expect one country of residence, one primary address, and one tax jurisdiction.

These assumptions work well for local customers. But when someone moves between countries or manages income internationally, these expectations quickly create expat banking problems.

Automated systems may interpret international activity as unusual behaviour rather than normal financial activity. Solutions designed specifically for banking for expats aim to address these structural limitations.

> When international activity looks like risk

Banks rely heavily on automated monitoring systems to detect fraud and ensure regulatory compliance. These systems analyse transaction locations, currency flows, and frequency of international transfers.

For people living abroad, these patterns may appear unusual. High levels of cross-border banking activity can trigger additional checks.

As a result, many people experience international banking issues, including temporary account restrictions, delayed transfers, and repeated document requests.

Modern solutions focused on international banking aim to simplify these global financial patterns.

Replace every card with one.

Connect your accounts to Bankeaz and choose in seconds which one your Unique Card spends from.

U N I Q U E

> Common banking challenges for expats

Globally mobile individuals often face similar financial challenges. One common problem is delayed international transfers. Payments may pass through several intermediary banks and compliance checks before reaching the recipient.

Another challenge involves repeated verification procedures. Banks may request proof of address or tax residency documents multiple times.

These frictions contribute to the growing number of expat banking problems experienced by people managing finances across borders.

According to the World Bank ↗, international remittances represent hundreds of billions of dollars every year, highlighting the scale of diaspora banking activity worldwide.

> A structural mismatch between global lives and local banks

The core issue lies in the structure of traditional financial systems. Most banking infrastructure was designed decades ago for customers living stable local financial lives.

But today, millions of people operate financially across borders. Remote work, international careers, and diaspora communities have created a world where financial lives are global.

This structural mismatch explains why banking for expats often feels unnecessarily complicated.

> The rise of global banking solutions

As global mobility increases, new financial services are beginning to address these challenges.

Digital financial platforms now support cross-border banking, international payments, and mobile customers worldwide. These services simplify international financial management and reduce friction caused by traditional systems.

Solutions designed for international banking and diaspora banking focus on transfers, multi-currency accounts, and financial tools adapted to global lifestyles.

______________________________________________________________________________________________________________________________________________________

> A new generation of banking for expats

As global mobility continues to grow, the limitations of traditional financial systems are becoming increasingly visible. Millions of people now live and work across borders, yet still face unnecessary expat banking problems.

New financial services designed for banking for expats aim to simplify cross-border banking, reduce friction in international transfers, and support global lives.

If you live between countries and want a banking experience designed for global mobility, you can join the Bankeaz waiting list to be among the first users when the service launches.

Bank without limits.

Open your Bankeaz account in minutes and manage your money across borders — simple and free.

B-Free

______________________________________________________________________________________________________________________________________________________

by BANKEAZ

On demand banking services for all

______________________________________________________________________________________________________________________________________________________

Learn more about Expat Banking

Global lives deserve simpler banking.

Download the BANKEAZ app for a 100% mobile banking experience. Available on iOS and Android.

Bankeaz is designed for people living between countries. Availability may vary depending on the user’s jurisdiction of residence.

The Bankeaz app is developed by Arcadia, a company currently being incorporated in Switzerland.

Bankeaz does not provide banking services in its own name. Financial services are provided by licensed and regulated partner institutions, in accordance with applicable laws and regulations.

Copyright © 2026 - Arcadia | Bankeaz - All rights reserved

Address

____________________

__________________________________________________________________________________________________________________________________________________

(- - -) - - - - - - - - - -

Zurich - CH

__________________________________________________________________________________________________________________________________________________

___________________________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________________________

Learn

____________________